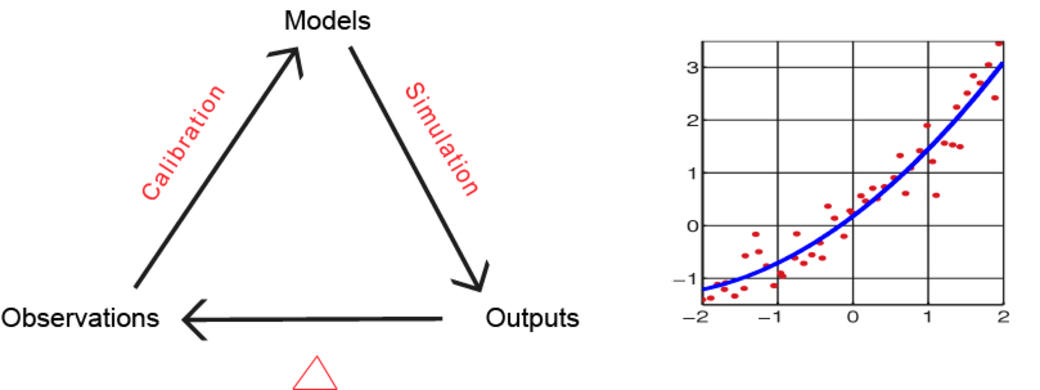

Calibration of Models

Calibration and identification of model parameters in models is major issue. The calibration of the bio-economic models can be carried out following different approaches. For some case studies, calibrations can derived from already existing stock assessment methods and economic data and models, in that case the way to couple theses models is a crucial question. In other case studies, specific integrated and bio-economic assessments are needed. This is generally obtained by fitting the model outputs to the available data.

The field of system identification and calibration uses statistical methods to build mathematical models of dynamical systems from measured data.

The calibration of models consists in estimating the value of parameters underpinning the model by fitting the observed outputs to the outputs induced by the model. The least square and maximum-likelihood methods are the most usual approaches. Kalman Filter can be also a very relevant method to estimate both the parameters and the state of a dynamic model for adaptive management in stochastic contexts.

Assume that the mechanistic model is described by the following discrete time equation

x(t+1)=f(x(t),c(t),β),

where x(t) stands for the state of the system, c(t) is the control of the system and β represents the parameters to identify.

The outputs of the system y(t) are functions of x(t) and c(t) as follow:

y(t)=h(x(t),c(t))

Consider that a sequence of past observations |

ydata(a), ydata(a+1),...,ydata(b) is available between times a and b

|

The least square method consists in minimizing the difference between the observed outputs y data(t) to the outputs induced by the model y(t)

|

min β Σt=ab|| ydata (t) - y(t)||2 |